Horizon Brief: A More Multipolar World

30 May 2026: Strait Stays on a Knife-Edge as Iran Deal Yet to Be Done — On the Radar, System Insights, and Recommended Reads

In this edition: Signal of the week; system insights; what I am reading; and one last thing.

Signal of the Week

Strait Stays on a Knife-Edge as Iran Deal Yet to Be Done

There were positive signs last weekend US and Iranian diplomats were edging toward a framework that could ease tensions around the Strait of Hormuz, after US President Trump had posted on his social media platform that an agreement had been “largely negotiated” and was awaiting finalisation, with a flurry of regional diplomacy involving Pakistan, Qatar, Saudi Arabia, the UAE, Turkey, Egypt, Jordan and Bahrain.

Subsequently, the Iranians reportedly poured cold water on the idea that a deal with the US was imminent, citing confusion in US positions and Israeli interference.

However, the US Secretary of State Marco Rubio struck a more measured note, telling a White House cabinet meeting: “Diplomacy is the first option”. But he reminded the president that he has other options available to him if that doesn’t work.

Still, the US reportedly conducted new military strikes against Iran this week in what were described as defensive in nature. Iran, meanwhile, said it had struck at a U.S. base in response.

Reports emerged Thursday, citing the American side, suggesting that a deal had been reached but had yet to be approved, with the Iranian side saying it had not been finalised.

Oil prices remained volatile this week as traders weighed up diplomatic progress towards a deal and fresh US and Iranian strikes. The international benchmark Brent crude price fell to just above $94 a barrel on Monday before rising the following day. By Friday afternoon, Brent oil prices were trading in a range of $87 to $92 a barrel.

We are not there yet. But if a deal does emerge to end this three-month conflict, it will likely be a negotiated accommodation rather than a return to the pre-war status quo, with both sides seeking something they can claim as a win.

The proposed 60-day framework deal reported last weekend would reportedly see Hormuz reopened without tolls, allow Iran to sell its oil, lift the US blockade on Iranian ports, with negotiations to follow on Iran’s nuclear programme later.

However, semantics still matter. An Iranian official reportedly said in Tehran this week that while “there is no toll” on the Strait of Hormuz, ships wishing to cross will likely be required to make some form of payment, such as an environmental charge.

Meanwhile, during the week, President Trump on his social media platform may have complicated matters further by requesting that the countries involved in the negotiations should sign the Abraham Accords, a set of agreements to normalise diplomacy between Israel and Arab states, and suggested Iran could be part of them.

As things stand, the broad direction of travel is clear, but the diplomatic outcome remains fluid, and the reporting remains mixed.

On the Radar

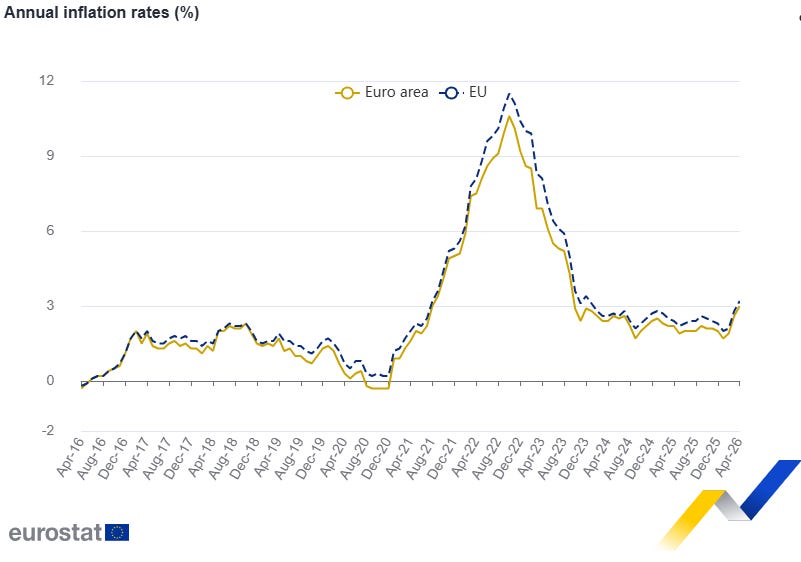

The upcoming ECB interest rate decision, scheduled for 11 June, is shaping up as a key macro event for the euro area. The meeting will set the near‑term cost of capital, influence the euro’s trajectory against the dollar, and indirectly affect the financing environment for larger European spending priorities, including defence.

That decision comes against a more difficult backdrop where external shocks are amplifying volatility. Reuters recently reported that ECB chief economist Philip Lane told Japan’s Nikkei that the bank will likely revise its inflation and growth forecasts next month due to the worsening outlook stemming from the Middle East conflict and persistently elevated energy prices.

In the bank’s last monetary policy statement at the end of April, it was explicitly stated that they were not pre-committing to a particular rate path. However, the sentiment in the marketplace signals that they will hike rates.

A majority of economists recently polled by Reuters now expect the ECB to hike rates in June, and nearly half expect another hike later this year. Only a few predicted three or more.

While it is still speculative, if there were a scenario of a hiking cycle that pushes the deposit rate significantly upwards, say closer to 3% by year‑end, there is a risk that the resulting tightening could sharply increase refinancing pressures for fiscally fragile member states, particularly Italy, one of the euro area’s largest and most indebted economies.

System Insights

Deal or no deal. US and Israeli military operations against Iran since February 2026 and subsequent Iranian action have raised much concern about oil and natural gas markets, with roughly 20% of the world’s maritime trade in crude oil and petroleum products normally passing through the Strait.

The Iran/Hormuz crisis is the most concentrated expression of what the Indian-American political author and columnist Fareed Zakaria once presciently called the “post-American world”, a world in which the United States still plays a pivotal role, but in relative terms it is not what it once was, because of “the rise of the rest”.

In such a world, one could say that the US still has sufficient power to start wars but increasingly appears to lack the power to resolve them unilaterally. Looking at the world through this lens, the role of multiple countries such as the Gulf states, Pakistan, and Turkey in the negotiations is a feature of an emerging multipolar order, not a temporary diplomatic oddity. Still, it also bears noting that, while the world is becoming more multipolar, with most of these brokers having greater voice, for now they remain embedded within, rather than independent of, a broader US-led security order.

As the conflict unfolded, official data shows that US inflation has been pushed to 3.8% annually in April 2026 (which is nearly double the Federal Reserve’s target of 2% as part of its dual mandate). This is largely on the back of increased energy costs. A workable deal would likely ease energy-cost pressures and reduce upside risks to inflation over the coming months. However, a collapse in negotiations could mean a resumption of conflict and send the international Brent benchmark price sharply upwards with potentially severe consequences for global growth in many sectors, from manufacturing to transportation and tourism.

Given the volatility of the geopolitical situation, with both sides trading strikes this week, a deal is still very much possible, but with fresh complications such as President Trump’s Abraham Accords curveball, it would be premature to bet on a single outcome. Events are moving quickly, so preserving optionality across both scenarios is best.

Hike or hold. That is the question on the ECB’s mind ahead of next week’s rate decision. The marketplace now leans toward a June hike. The Eurozone’s central bank held its deposit rate at 2% for the third consecutive meeting on 30 April, but euro area inflation had jumped to 3% in April, driven by higher energy and service costs, while euro area GDP rose 0.1% quarter on quarter in Q1 2026 and 0.8% year on year, after recording 1.3% year-on-year in the previous quarter.

The ECB’s Governing Council considers that price stability is best maintained by aiming for 2% inflation over the medium term. The current inflation numbers are enough to keep pressure on policymakers.

With inflation rising and growth remaining weak, the euro area faces a familiar policy trade-off: tighten further to preserve price stability, or hold steady and risk allowing inflation to remain sticky.

The ECB is not pre-committing to a particular path, but market expectations have tilted toward a June hike; the key question is how far the Governing Council is willing to go if inflation remains elevated, and how it will manage transmission risks if sovereign stress reappears.

If a tightening cycle did sharply increase refinancing pressures for fiscally fragile member states, the ECB does have tools at its disposal, such as the Transmission Protection Instrument, but there are also eligibility criteria that member states would have to fulfil.

What I’m Reading

China’s Influence. Tobias Gehrke argues in an article for the European Council on Foreign Relations that China no longer needs to use economic coercion against Europe because just the threat of its expanding coercive tools is enough to make the EU self‑censor and abandon necessary industrial and trade defences, thereby achieving Beijing’s objectives at effectively a zero cost. How China’s silent coercion has Europe sanctioning itself – European Council on Foreign Relations

Global Capital. A new World Bank analysis by Arlan Brucal, Kanako Nannichi, and Francisco Aguilar Cisneros shows how global capital is converging on AI, digital infrastructure, and clean energy, the technologies set to define the next economic period. FDI is no longer chasing growth; it’s creating it, as investors bet on future demand rather than current income. Where global investment is headed: what the data say about digital innovation and the energy transition

A G-2 World. Following the US–China summit in Beijing, Zheng Wang argues in Foreign Affairs that a new G‑2 world is taking shape: one in which neither Washington nor Beijing can dominate or exclude the other. Both have discovered the limits of coercion, giving rise to an equilibrium of mutual denial. Taiwan is the most volatile fault line. The strategic task ahead is managing a tense but durable coexistence. The G-2 Reality: America and China Cannot Dominate or Exclude Each Other

Culture and power are locked in a constant negotiation, drawing on ideas from political science, political economy, and management practice. This episode of the Forces and Signals podcast sets out what it actually takes to shift culture in a way that lasts

Culture Follows Power, If It Earns It

Culture is often treated as the soft side of organisational and societal life, important, perhaps, but secondary to strategy, structure, and resources.

One Last Thing

European Exports to the US Plunge 30% as Tariff Tensions Hit Trade Data

The transatlantic trade shock is now showing up in official EU trade statistics, with implications for EU corporate earnings, supply chain strategy, and geopolitical risk pricing.

The latest Eurostat data confirms that EU exports to the United States plunged 30.4% year-over-year in Q1 2026, falling to €119.4 billion, the largest drop among major trading partners. In the first quarter of 2026, the EU also imported 5.7% less from the US.

Overall, the EU trade surplus with the US narrowed to €34 billion from a peak of €80 billion in Q1 2025, an adjustment that is likely to be welcomed in Washington, where bilateral trade balances are a key focus of the Trump administration’s economic policy.

Part of this decline reflects a distorted comparison base, as US importers front-ran tariffs in early 2025. However, even after accounting for this, the broader trend points to weakening transatlantic trade momentum, though it is still too early to conclusively pronounce a structural shift. On a quarterly basis, EU exports to the US actually rose modestly (3%) in Q1 2026, and it’s important to note that the US remains the EU’s largest export market, accounting for 18.6% of total exports.

Time will tell what the next twelve months will bring, but there are two scenarios to consider. Trump has recently threatened a scenario of much higher tariffs on EU goods by July 4, 2026, but recent progress towards formal European institutional approval of the Turnberry Framework agreement suggests that the previously agreed 15% tariffs scenario is more likely to prevail.

The data for the second quarter of 2026, due in August, should provide further clarity on whether this is a temporary adjustment or the start of a more durable realignment.

Thoughts shared here are intended for discussion and knowledge only, not financial, investment, or legal advice. Always chat with your advisors first. - Horizon Briefing returns on 18 July 2026.