Horizon Briefing: Beijing Talks and EU Deadline

16 May 2026: Trump in Beijing, No Significant Breakthroughs — On the Radar, System Insights, and Recommended Reads

In this edition: Signal of the week; system insights; what I am reading; and one last thing.

Signal of the Week

Trump in Beijing, No Significant Breakthroughs

U.S. President Donald Trump travelled to Beijing this week to meet with Chinese President Xi Jinping, with the expectations around the highly anticipated summit tempered by the ongoing war in Iran.

It was President Trump’s first trip to China since 2017 and his first face-to-face with Xi since their October 2025 summit in South Korea.

Why it Matters:

Given the geopolitical context in which neither side fully controls, this was arguably expected to be one of the most consequential bilateral meetings between the US and China in some time.

Any useful cooperation between the U.S. and China is good for both countries but also for international stability, particularly on reopening the Strait of Hormuz, which could offer near-term relief to international oil prices.

While there were no significant breakthroughs at this summit, some trade business was completed, and President Xi has been formally invited to visit the US in September.

Key Details:

President Trump’s visit was originally due to take place at the end of March but was postponed by six weeks because of the ongoing war with Iran.

China is reportedly Iran’s largest trade partner and the top buyer of its oil, according to recent US and industry data. That means Beijing has skin in the game and should be expected to wield significant influence.

During the summit, China and the US reportedly agreed that the Strait of Hormuz should remain a free waterway and the Iranians shouldn’t have a nuclear weapon, according to reports citing a White House readout.

However, while there may be some overlap of interests, it would be hard to argue that this is strategic alignment. On the last day of the visit, the Chinese Foreign Ministry reportedly issued a blunt statement saying the conflict, which should never have happened, should not continue.

China has, however, reportedly agreed to buy 200 Boeing aircraft and potentially agricultural products from the US in a signal of some trade progress. However, it is still not clear if Nvidia can sell more of its advanced chips to China, despite its CEO travelling among several other titans of corporate America on the trip.

Sources: CNBC, CSIS, Atlantic Council Horizon 9/5/26 CBC News Reuters Reuters+1 USCC World Visualised

On the Radar

4th July Trade Ultimatum for the EU

After U.S. negotiators met their EU counterparts in Europe last week and agreed to reconvene after more than six hours of talks, President Trump subsequently posted on Truth Social that he had given the European Union until 4 July to “fulfil their side” of the Turnberry trade agreement, warning he would raise tariffs to “much higher” levels if Brussels fails to act after a “great call” with European Commission President Ursula von der Leyen.

Why it Matters:

The 4 July deadline, America’s 250th birthday, imposes a forced timeline that could strain one of the world’s largest bilateral trading relationships at a moment when Europe is already vulnerable to energy‑driven inflation and spillovers from the US‑Israel‑Iran war.

Legal and political constraints on both sides make the scenario uncertain. U.S. courts have questioned the administration’s tariff authority, while an appeals administrative stay is allowing collection of the 10% levy for now, leaving domestic legal outcomes as a live wildcard for markets and policymakers alike.

Meanwhile, if the Turnberry package were to unravel, Brussels has an untested retaliatory option. The EU could use its anti-coercion instrument (the so‑called “Bazooka”), which is a trade tool that entered into force in 2023 but has never been deployed which allows for a range of actions from prohibiting the export of strategic goods, withdrawing protection from intellectual property, to excluding business from European tenders, though it must also be noted that political thresholds for its use are high and its deployment would surely be an unprecedented move in the transatlantic relationship.

Key Details:

Following her call with President Trump, the European Commission President Ursula von der Leyen signalled progress from the European perspective, writing on X that “good progress is being made towards tariff reduction by early July,” reflecting optimism from Brussels even as technical and political work continues.

Those sentiments echo the European Parliament’s chief trade negotiator, Bernd Lange MEP (S&D, DE), who said after the second round of negotiations with member states that EU lawmakers and governments had made “good progress”, but added that “there is still some way to go”, underscoring remaining legislative and intergovernmental tasks before implementation can be completed.

Trade policy is an exclusive EU competence, but completing the Turnberry package requires final approvals in the Council of the EU (by the member states) and, where relevant, national procedures, which can make its implementation politically and procedurally complex.

Complicating matters on the American side was the U.S. Court ruling on 7 May against the Trump administration’s use of Section 122 to justify a global 10% tariff that exceeded its authority under that law; an appeals court has subsequently issued an administrative stay allowing collection to continue while the appeal proceeds, so the legal outcome remains uncertain and could constrain U.S. trade policy.

Sources: President Trump on Truth Social EC President VDL on X Time Le Monde WSJ European Parliament European Parliament+1

System Insights

Power Politics

The Trump‑Xi summit in Beijing signals a clear tilt towards managed, bilateral competition, signalling a shift toward institutionalised rivalry between the two largest economies rather than a return to open multilateral globalisation.

International relations theory is useful here. Seen through the lens of the American international relations theorist Graham Allison’s “Thucydides Trap,” the summit underscores the structural tension between China as the rising power and the US as the entrenched one. During the summit, the Chinese president referenced this concept and made a point of calling on both parties to focus on stability and avoid falling into this trap and instead gain from cooperation. He also reportedly warned that if the Taiwan question is not handled properly, the two countries will have clashes and even conflicts, putting the entire relationship in great jeopardy, according to the Chinese state news agency Xinhua.

On the other hand, the summit also reflected pragmatic restraint, with both sides reported to have reached “new common understandings” and to have agreed to strengthen their communication on international and regional issues in the coming years.

This resembles an institutionalisation of rival management, where rival great powers are institutionalising channels of communication precisely because the costs of accidental escalation (in trade, AI, Taiwan, or energy) have become systemically unacceptable. The Iran war seems to have accelerated a logic in which both Washington and Beijing have economic incentives to reopen the Strait of Hormuz, creating some shared interests.

This bilateral relationship is often described by think tanks as the world’s most important and consequential, and both President Trump and President Xi described it in those terms this week, with the Chinese president adding that both sides should never mess it up. However, the value of this week’s summit lies less in headline deals than in what it signals about how both sides will balance risk containment while preserving leverage over each other in a high-stakes rivalry.

This week, there was little evidence of overt escalation in tensions between the two countries, which projects a certain degree of temporal stability to their domestic audiences and the wider world. President Xi has been formally invited for a visit to the US in September. However, behind the pageantry and friendly social veneer, there are significant differences, such as the reported Chinese foreign statement on the Iran war that should never have happened and should not continue, on the final day of the Summit.

Weaponisation of Trade Interdependence

Trump’s 4 July ultimatum to the EU closely reflects what political scientists today would describe as “weaponised interdependence”, the use of structural economic dependencies as geopolitical leverage.

The EU is caught in a dilemma with limited room for manoeuvre. It could comply with Washington’s timetable to preserve its market access; it could resist to preserve its democratic procedures and institutional credibility; or it could retaliate using the untested “Bazooka” anti-coercion instrument, but risk further escalation.

The diversity of interests and opinions on what to do next, from French President Macron’s recent assertive stance on strategic autonomy to the more accommodating approach of some Central European leaders, complicates Brussels’ ability to present a unified response because different member states operate with different interests and incentives.

Meanwhile, a U.S. court ruling and pending appeals create a legal wildcard, which, depending on the outcome, could ultimately constrain Washington’s tariff options more than a European diplomatic pushback.

So, the July 4 deadline is the next critical inflection point, but the outcomes are likely to be messy and incremental. Some have referred to the trade agreement as lopsided; the agreed tariff structure does serve American interests better than before, but the EU hoped this concession would provide more predictability and stability. Complete implementation of the Turnberry package by America’s Independence Day is politically possible but still procedurally challenging. A phased or sequenced implementation (partial ratification followed by gradual measures) may be the most plausible compromise.

Meanwhile, European export-heavy industries, from German cars, French wine and spirits, to Italian luxury goods, remain in the direct line of fire during these trade tensions. If the EU chooses to use the Bazooka in the event of failed talks, US businesses reliant on EU procurement or exports could face tangible disruption; conversely, if Washington’s tariff authority is curtailed by the courts, political threats may have limited persuasion power.

What I am Reading

Digital Euro: Duncan Weldon writes in the Chicago Booth Review that a digital euro is less about improving payments for Europeans and more about safeguarding Europe’s monetary sovereignty as foreign (especially US) payment systems and dollar-based stablecoins gain influence. The underlying driver is geopolitical and systemic risk, not consumer convenience. Does the EU Need a Digital Euro? | Chicago Booth Review

Transatlantic Alliance: Philip Stephens in his Substack, Inside-Out, paints a picture of a paradigm shift that is underway in the transatlantic alliance as a coherent geopolitical system. He argues that the post‑1945 Atlantic alliance has effectively ended because the trust, power balance, and shared purpose that once bound the US and Europe have collapsed, leaving only a thin, transactional relationship in its place. America has left the West

Global Supply Chains: Nadiya Albishchenko, in an article for LSE Business Review, argues that global supply chains are breaking down because they were built for stability and transparency, but now operate in a disruptive world defined by geopolitical volatility, opaque routing decisions, and collapsing visibility, forcing firms to make high‑stakes decisions with incomplete information. The issue is whether systems are now capable of maintaining control. What Happens When Supply Chains Go Dark

One Last Thing

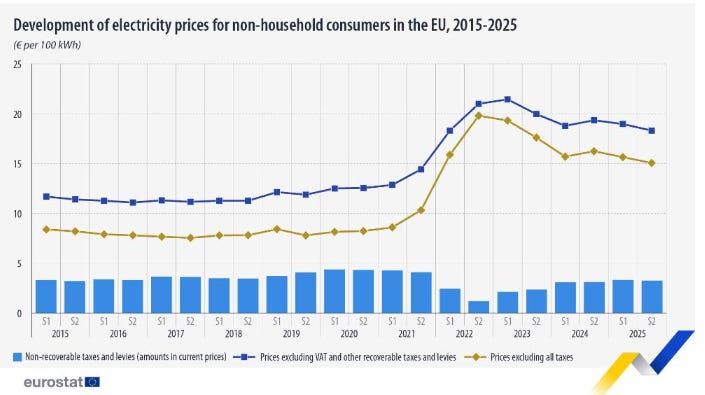

The High Price of Electricity in the EU

New data published this week by Eurostat, the statistical office of the European Union, showed that in the second half of 2025, the average price of electricity for non-household consumers in the EU was €18.37 per 100 kWh.

While prices have shown a mild downward trend since the second half of 2023, the spread across member states remains wide, reflecting structural differences in national energy systems. The highest prices in the second half of 2025 were in Ireland (€25.52 per 100 kWh), while the lowest were in Finland (€7.48). Germany, a major industrial economy, was also among the more expensive markets (€22.64).

Electricity prices for non-household consumers in the EU are significantly higher relative to those of its major economic peers, such as the US and China, over a similar period. For many European businesses consuming 500–2,000 MWh/year, electricity is a core input cost, so such higher prices are a drag on EU competitiveness, especially for energy-intensive sectors. This could lead to them delaying electrification decisions across more of their business processes, where electricity is a meaningful process input. The challenge for the EU’s leaders is to find the right balance between decarbonising the economy while also keeping industry competitive, which is not an easy task when power prices stay elevated.

As always, thoughts shared here are intended for discussion and knowledge only, not financial, investment, or legal advice. Always chat with your advisors first.